Daily Quizzes

Mock Tests

No tests attempted yet.

Select Category

GST Council to Discuss Reducing Items in 12% Slab

Overview: In its upcoming meeting scheduled for July 2025, the GST Council is expected to discuss removing the 12% tax slab to simplify the GST structure. The move could shift items to either the 5% or 18% bracket, impacting pricing and input tax credits. Tax relief for service intermediaries is also under discussion, which may boost India’s export competitiveness.

The GST council will deliberate on the move to cut down items in the 12% tax bracket in their next meeting that is expected to be held in July 2025 due to held-up meetings. The argument that stands out as one to discuss is whether to eliminate the 12%. slab as part and parcel of the rationalization and simplification of rates. Taxation of service intermediaries is also on the agenda of the council which may relieve the sector of heavy taxation. Such verdicts have the potential to introduce tax waiver measures that run into thousands of crores and which will have an effect on business and consumers alike on an Indian scale.

Context

-

In its next meeting, the GST Council will discuss the possibility of reviewing the 12% slabs and also, on the taxation of service intermediaries.

-

The changes may result in reduced taxation rates and even magnificent reprieve to the service sector.

Key points

An Meeting Agenda:

-

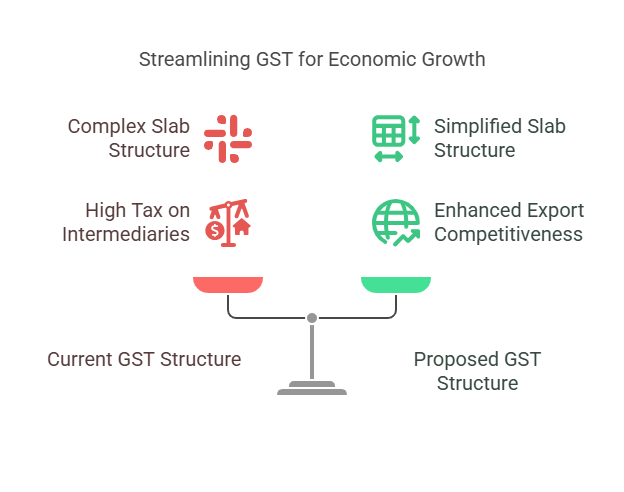

Rate Rationalization:

-

Recommendation of reducing or removing this 12 % GST slab

-

To simplify to four principal slabs: 0%, 5%, 18%, 28%

-

-

Taxation Service Intermediaries:

-

Reconsideration of 18% GST on intermediaries that will provide the service to clients abroad

-

May relieve and enhance export competitiveness harmonizing tax levels

-

Effects of a Reduction/Removal of the 12% Slab:

-

The 12% items can be transferred to 5% or 18% and compliance made easy

-

May limit the availability of input tax credit (ITC) by manufacturers

-

Undercharge on utilitarian products such as toothpaste and soap

Significance

-

Manufacturers Worries:

-

ITC loss in case of shift to 5% slab

-

Possible rise in the input costs

-

The variation on sectors could be high with FMCG and consumer goods being the highest affected.

-

-

Relief in Service Sector:

-

Negotiating the relaxation of tax regulations of service intermediaries

-

Will lower the total tax liability and increase outsourcing business internationally

-

Conclusion

The next meeting of the GST council can bring a significant simplification to the Indian taxation system, as the council is considering dropping the 12 percent tax bracket and changing the taxation on service intermediaries. These resolutions may help minimize the taxation rates thus ensuring that the GST structure would be effective and also recognize the objections of the industries regarding the input tax credits. Nevertheless, these reforms should not be one-sided but should strike a balance between the needs of the consumers, manufacturers and the service sector so as to pioneer a long-term economic increase.

Related Current Affairs

From 1776 to 2026: Adam Smith's Lessons for the Global Economy

From 1776 to 2026: Adam Smith's Lessons for the Global Economy SBI Strongest Indian Bank; HDFC Bank Leads in Brand Value

SBI Strongest Indian Bank; HDFC Bank Leads in Brand Value India’s New GDP Series: A Game-Changer for Accurate Economic Growth Measurement

India’s New GDP Series: A Game-Changer for Accurate Economic Growth Measurement Kerala Presents India’s First Elderly Budget

Kerala Presents India’s First Elderly Budget US Changes India Trade Deal Statement, Sparking Confusion

US Changes India Trade Deal Statement, Sparking Confusion Taxpayer Base More than Doubled in the Last Decade

Taxpayer Base More than Doubled in the Last Decade Walmart Becomes First Retailer to Hit $1tn Market Value

Walmart Becomes First Retailer to Hit $1tn Market Value India's Union Budget FY 2026-27: Key highlights

India's Union Budget FY 2026-27: Key highlights Tripura Gramin Bank Launches India’s First Solar-Powered ATM Van

Tripura Gramin Bank Launches India’s First Solar-Powered ATM Van India Emerges as World’s Largest Rice Producer

India Emerges as World’s Largest Rice Producer